The crypto market is in bloom, and innovation is flourishing. Virtual loans let users pledge their assets to borrow fiat or cryptocurrencies. This peculiar form of lending merges conventional finance with cutting-edge technologies based on blockchain. Both borrowers and lenders make their assets work without selling them.

Crypto loans are more accessible and flexible than old-school bank loans. They do not require credit checks, as crypto collateral is sufficient. Funds are distributed almost instantly, without lengthy verifications. Collateralization has gained popularity over the past few years, and the market is booming as enthusiasts hunt for yield. According to Forbes, the total loan originations have exceeded $10 billion.

At the heart of this trend, there is a desire to access liquidity instantly without any hurdles. Users can satisfy cash needs without diverting their assets. As borrowers, they remain entitled to future profit from their coins.

Platforms offering such loans are bursting onto the scene. The crypto interest account on coinloan.io stands out due to attractive LTV, low-interest rates, and free withdrawals. Here are five systems with the best conditions overall:

|

Platform |

LTV |

Interest rate |

Origination fee |

APY |

Type |

|

CoinLoan |

50%-70% |

4.95%-11.95% |

1% |

Up to 12.3% (8 assets) |

CeFi |

|

NEXO |

15%-30% |

6.9% - 13.9% |

- |

Up to 20% (MATIC only) |

CeFi |

|

BlockFi |

20%-50% |

4.5%-9.75% |

2% |

Up to 9.5% (USDT) |

CeFi |

|

YouHodler |

50%-90% |

16.22% - 25.55% |

1% |

Up to 12.3% (Tether) |

DeFi |

|

Celcius |

25%-50% |

1% - 8.95% |

- |

Up to 17.78% (SNX with Platinum level) |

DeFi |

These loans work similarly to conventional bank loans with collateral. If you own crypto, you can pledge it to secure a loan in fiat or crypto, depending on the platform. Collateral protects the interest of the lender. At the same time, it is an innovative economic system shaped by algorithms and smart contracts. Unlike traditional banking services, crypto loans are decentralized and autonomous.

Another advantage is the absence of credit history checks. Crypto-backed loans are accessible for users with thin credit files and low scores. Improving a credit history takes months or years, while crypto loans are a few clicks away.

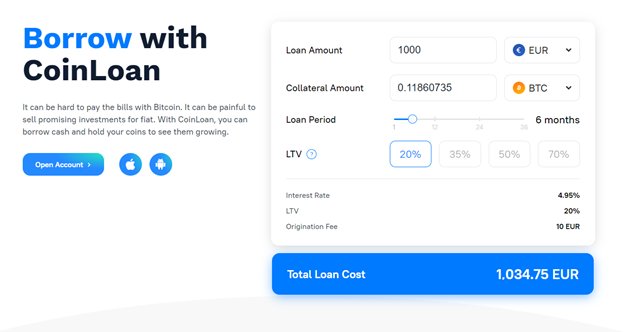

The key terms for a borrower are interest rate and LTV (loan-to-value) ratio. The latter shows how much crypto you must pledge to borrow a certain amount. If the collateral value falls, the borrower is asked to add more of it to restore the proportion. For example, a platform may offer LTV of 50% or 70% for different types of loans.

Crypto loans appeared as a solution for users who chose hoarding over selling. They can boost the productivity of their assets while maintaining ownership. However, this dimension of the lending is still relatively new. If you are still skeptical about using crypto for collateral, read on.

These transactions let users lend and borrow crypto on exchanges or specialized platforms like CoinLoan. Interest is incurred at an agreed rate over the life of the loan, just like in the conservative financial system. Platforms work as intermediaries connecting lenders to borrowers. Every loan agreement includes three players:

Individual users deposit fiat or crypto, which are used for loans. For lenders, this is an opportunity to make assets work without selling them. They make a passive income, getting their money back with interest.

All systems supporting landing are divided into centralized (CeFi) and decentralized (DeFi). All of them are intermediaries. Platforms that connect borrowers to lenders directly are known as P2P platforms. Learn about the differences between these types below.

Any individual or company that owns crypto-assets can take out a loan. For example, this is a quick source of funding for startups. Borrowing with crypto is a cost-effective and straightforward way to finance any purchase. On CoinLoan, there are no lock-ins, fines, or hidden fees.

Using Bitcoin for payments is complicated, and it is painful to sell the coins. Loans solve this problem, as users can borrow cash while still owning their assets. After repaying the loan with interest, they get their collateral back.

Crypto loans can be used for absolutely any purpose, big or small. You can refinance debt, buy a home or pay for education. This is a universal instrument for individuals and companies. They secure capital quickly with modest interest rates and still profit from their digital assets.

The absence of credit checks makes these loans more accessible than conventional services, even payday loans. A crypto arrangement could be a lifesaver in emergency situations. Credit ratings do not matter. You won’t be asked for proof of employment or income to qualify, either.

These loans are also widely used for portfolio diversification, as lenders can use passive income from their assets to purchase other coins or tokens.

The absence of credit checks and universality are not the only advantages of crypto lending. These loans are more flexible and faster than conventional services. You can forget about such hurdles as credit score checks and lengthy verification procedures. Sometimes, credit scores plunge due to bad luck or mistakes in a credit report. Restoring them takes forever.

Crypto loans are available 24/7, efficient, and lightning-fast. To qualify for a loan, you only need to verify your identity and provide collateral meeting the requirements. What’s more, this innovative system gives users more power over their finances. They can select loan terms matching their situation and repay sooner without penalties. You need just a few minutes or hours to secure a loan.

Crypto lenders earn interest. On the surface, the system is similar to a savings account. In offline finance, you stash some money while the bank or credit union pays interest on the balance. The institution may use your funds to provide loans to other clients. The same happens in the crypto world, but the rates are much higher — for example, depositing a stablecoin like USDT or PAX on CoinLoan brings up to 12.3% APY.

Lenders who choose reliable platforms reap multiple benefits. First, crypto collateral is liquid, so transactions are quick. Secondly, they are protected from excessive volatility of the collateral, thanks to LTV. On some platforms, borrowers may be asked to collateralize the entire loan amount or even more. Finally, there is no lengthy paperwork or verification hurdles. Everything is digitized, streamlined, and quick.

The constant debate between proponents of centralized and decentralized finance is one of the reasons why crypto loans can be confusing for beginners. Decentralization is part and parcel of all cryptocurrencies, but platforms facilitating the transactions are very different.

Both systems aim to create a world of decentralized finance, but they use different methods to achieve this goal. The debate boils down to one question: can we totally rely on technology for all transactions and verifications?

CeFi platforms are managed by fintech companies that borrow some of their methods from conventional financial institutions. Users complete the Know Your Customer (KYC) procedures to confirm their identities, and digital assets are protected by custodial services. At the same time, such platforms can form alliances with conventional capital providers to negotiate loan agreements.

On the upside, lenders of popular assets like Bitcoin or Ethereum enjoy higher returns and more security. However, the transaction fees may be substantial, and some users are not happy to share their identifying information.

Decentralized counterparts do not use KYC or custodial services, as they rely on technology to manage all aspects of transactions. Maker is a notable exception, as this DeFi system sets the interest rates for users. On other platforms, they vary depending on the supply and demand for each asset. This explains the high changeability of interest rates.

The absence of centralized control can be seen as an advantage or disadvantage. Some users praise DeFi, as these systems are quick and more accessible thanks to the absence of verification barriers. At the same time, the volatility of interest rates and lack of unitary clarity are problematic.

Both models support the evolution of crypto finance through quick transactions, impressive APY, and growing infrastructure. In comparison with banks, they provide more attractive rates for lenders and borrowers. Together, CeFi and DeFi promote the secure future of finance. At the same time, DeFi is still catching up in terms of usability and security, and it is most attractive to early adopters.

Despite all of its merits, the crypto landing has some inherent risks. After all, it is a new form of finance connected to volatile assets. Cryptocurrencies are known for their rapid ups and downs. Dramatic fluctuations are favorable for investors and sellers, but they complicate the situation for borrowers. They must accept the risk of adding more liquidity if their collateral depreciates. When it drops below the agreed LTV, they have to boost it.

Users of CoinLoan can check the status of their collateral at a glance. Their personal dashboard shows changes that occurred throughout the loan term. There are graphs for both LTV and collateral value. In the negative scenario, the collateral value drops while LTV rises. Once it reaches 80%, the user is informed of the liquidation risk to take action. There are three options:

Therefore, borrowers should keep track of their asset value. The liquidation systems have proven to work well, so lenders keep their investments while borrowers have an opportunity to prevent liquidation.

Speaking about loans on the DeFi platforms, they include risks stemming from the nature of decentralized finance. There, both lenders and borrowers completely entrust technology (smart contracts) with managing their transactions. All financial flows are governed by computer code, so it is theoretically possible to exploit such systems.

Currently, crypto lending is dominated by users with an in-depth understanding of the digital currency markets. It is not a settled or static sector, and its further development largely depends on changes in government regulation and oversight. If crypto accounts are eventually deemed securities, this will open the platforms up to a whole new spectrum of registrations and disclosure requirements for investor protection.

As more and more innovative solutions are expected in the crypto market, the average user will need to make decisions carefully. So far, no universal market standard has been developed, so crypto lending is still the wild west.

To choose an optimal crypto loan, look beyond the interest rates. Consider the LTV ratio, the repayment schedule, the quality of customer support, and security procedures. The yields dwarf those of conventional bank accounts. Yet, from a legal perspective, these services reflect traditional forms of commercial lending.

The industry is growing fast. For example, Celsius claims to have over $20 billion worth of deposits, while BlockFi boasts more than $10 billion. Crypto loans offer lenders a steady source of returns, considering the volatile nature of the market. However, it remains to be seen if digital loans can overshadow the conventional industry.

Crypto loans are a win-win for borrowers and lenders. They let them make their assets without letting them go. You do not need to sell your prized bitcoins to get a loan, as collateral returns after repayment. Meanwhile, lenders enjoy a high annual yield and guaranteed protection thanks to LTV. Even despite the absence of credit checks, they have peace of mind.

Popular platforms allow switching between assets and unlock lower interest rates in comparison with bank loans. You can buy Bitcoin and pledge it to borrow another coin or fiat without leaving the system. Convenient dashboards and instant notifications help borrowers keep an eye on their collateral. At the same time, crypto loans are still affected by market volatility, and LTVs vary.

Comments

No comments on this item Please log in to comment by clicking here